Introduction

Many people know their credit score is important, but few truly understand what has the biggest impact on it. Some believe income is the main factor, while others think opening many credit cards will help. In reality, credit scores are built around specific patterns in how you manage borrowed money over time.

Understanding what affects your credit score the most allows you to focus on the habits that truly matter. Small financial decisions made consistently can have a larger effect than people expect. When you know where to pay attention, improving your credit becomes much more manageable.

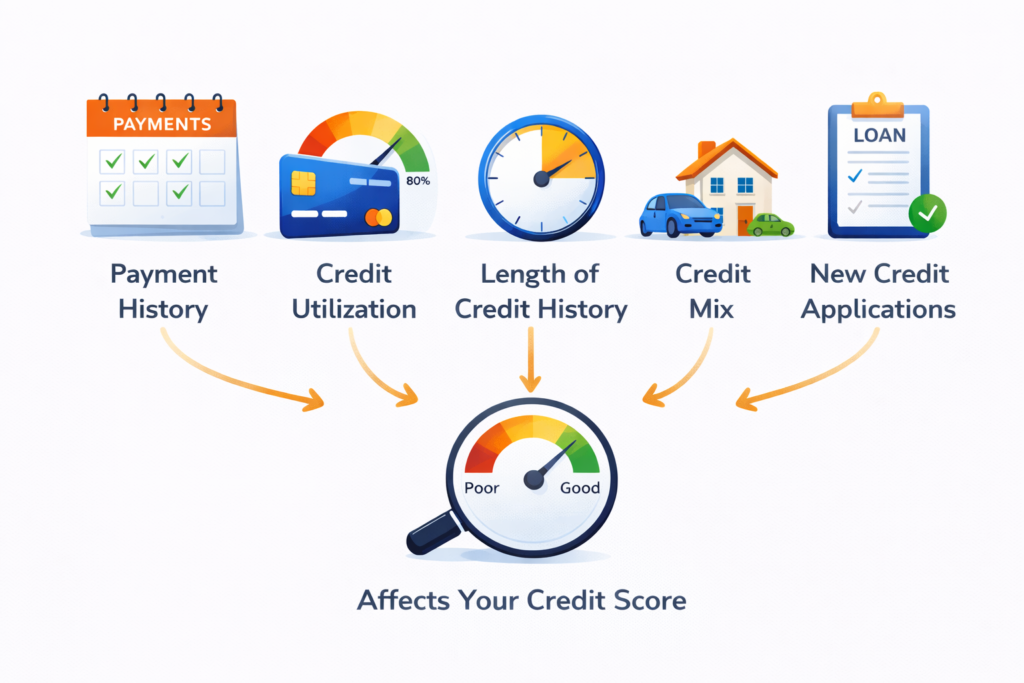

Payment History Is the Most Important Factor

If there is one element that carries the most weight, it is whether you pay your bills on time. Payment history shows lenders how reliable you are when it comes to meeting your financial obligations.

Each time you make a payment by the due date, you build a record of responsibility. On the other hand, late or missed payments can lower your score, especially if they are more than 30 days late and reported to credit bureaus. More serious issues, such as accounts sent to collections, can have an even stronger negative impact.

A good way to protect this part of your score is to set reminders or automatic payments. Even paying at least the minimum on time can prevent damage. Consistency matters more than the size of the payment.

Credit Utilization and How Much You Owe

Credit utilization refers to how much of your available credit you are currently using. This is another major factor that affects your credit score.

For example, if you have a credit card with a $1,000 limit and you carry a $900 balance, you are using 90% of your available credit. This high usage may signal to lenders that you are financially stretched. Lower balances compared to your limits show that you can manage credit without depending on it too heavily.

A common guideline is to keep your usage below 30% of your total available credit. Lower than that is even better. Paying down balances can quickly improve this part of your credit profile.

Length of Your Credit History

The age of your credit accounts also plays a role. Lenders prefer to see a long track record of responsible credit use. Older accounts show stability and give lenders more information about your financial behavior over time.

Closing old accounts can sometimes reduce the average age of your credit history, which may slightly affect your score. Keeping older accounts open, especially if they have no annual fee, can help maintain a stronger credit profile.

New Credit Applications

Applying for new credit can also influence your score. Each time you apply for a credit card or loan, a hard inquiry may appear on your report. Too many applications in a short period can make lenders think you are taking on too much debt or facing financial difficulty.

Spacing out applications is usually a safer approach. Opening new accounts occasionally is normal, but frequent applications may have a temporary negative effect.

Credit Mix and Types of Accounts

Your credit mix refers to the different types of credit you have. This can include credit cards, auto loans, personal loans, or student loans. Managing different types of credit responsibly shows lenders that you can handle various financial obligations.

While credit mix is less important than payment history or utilization, it still adds to the overall picture. However, you should not open new accounts just to improve this factor. Responsible use is more important than variety.

Factors That Do Not Directly Affect Your Score

There are many myths about credit scores. Your income, job title, age, or bank balance do not directly determine your score. You could earn a high income but still have a low credit score if you miss payments or carry high balances.

Credit scores focus on behavior, not personal background. Lenders want to know how you manage borrowed money, not how much you earn.

A Real-Life Comparison

Imagine two people. One always pays bills on time and keeps balances low. The other often pays late and uses most of their credit limits. Even if the second person earns more money, the first person is likely to have a higher credit score. This shows that habits matter more than income.

Final Thoughts

Your credit score is shaped mainly by a few core behaviors: paying on time, keeping balances low, and avoiding too many new credit applications. These habits build trust with lenders and improve your financial reputation over time.

Improving your credit score does not require complicated strategies. It comes down to consistency and responsible credit use. By focusing on the factors that matter most, you can gradually strengthen your credit and open the door to better financial opportunities.

Final Thoughts

Your credit score is mostly influenced by simple habits: paying on time, keeping balances low, and avoiding too many new applications.

Small, consistent actions over time can have a bigger impact than people expect. Understanding what affects your score gives you more control over your financial future. You can check more information on these pages:

Experian – What Affects Your Credit Score

MyFICO – How Scores Are Calculated (payment history 35%, amounts owed 30%, etc.)

Pingback: What Happens If You Miss a Credit Card Payment?

Pingback: What Lenders Consider Before Approving a Loan